Crop Report 2021/2022

Santos, January 6th, 2021.

Dear Coffee Friends and Partners,

Firstly, we’d like to wish you all a prosperous and healthy 2021.

And what a year 2020 has been, definitely one for the futury history books. When we look back at this time last year, as we were compiling our Brazilian 2020/2021 crop estimates, is when the coronavirus began spreading globally, which at the time appeared to be a remote threat to our way our life. A year on, the virus has pretty much reached all corners of the globe and touched each and everyone of us in different ways. While there is plenty of optimism as vaccines are being rolled out worldwide, this is something that will continue to be part of our day-to-day lives troughout the better part of 2021.

The big question lingering in everyone’s mind is what has all this done to global coffee demand. We all agree that there have been shifts in consumption channels (i.e. out-of-home to in-home, etc), and that there is a general impact on demand, but the truth is, the answer to this is far from clear. Having said that, the focus of this report will not be on demand but on our Brazilian green coffee production and exports estimates.

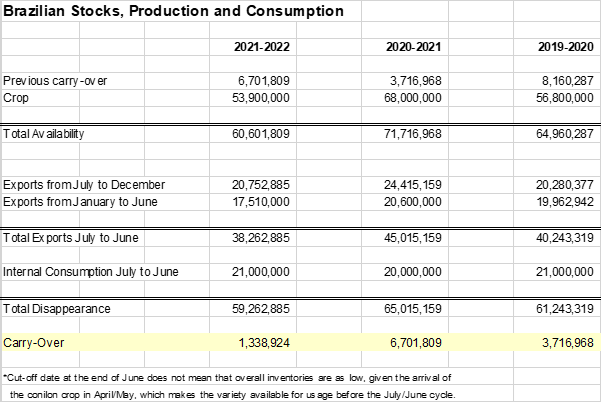

Looking back to our crop report from a year ago, we maintain our 2019/2020 estimates at 56.8 million bags, split 38 for Arabica and 18.8 for conilon. With 40.2 million bags of exports during the crop cycle and 21 million bags of internal consumtion, that leaves a carry over of 3.7 million bags coming into this current season.

The expectation coming into the current 2020/2021 was already that of a big crop. In last year’s report we estimated 67.7 million bags, being 48.25 for arabica and 19.45 for robusta. Now we are just past the halfway point of the season and we’ve made some minor adjustments to both our arabica and conilon estimates.

For the current 2020/2021 season, we are estimating a total crop of 68.0 million bags, being 50.8 million bags for arabica and 17.2 million bags for robusta. In other words we have increased our arabica estimate by 2.55 million bags and reduced our robusta estimate by 2.25 mln bags, leaving a net increase of 300 thousand bags.

Exports have continued to break records with Brazil shipping 24.4 million bags in July-December 2020 period, and 44.4 million bags during the calendar year (Jan-Dec-2020). Jan-21 export registrations are starting to indicate that this pace will start to slow, and as a result we are forecasting a further 20.7 mln bags of exports during the Jan-June 21 period, reaching a total export figure of approximately 45.1 mln bags for the full July20-June21 crop cycle. Leaving us with a carry-over for 20/21 of 6.6 million bags.

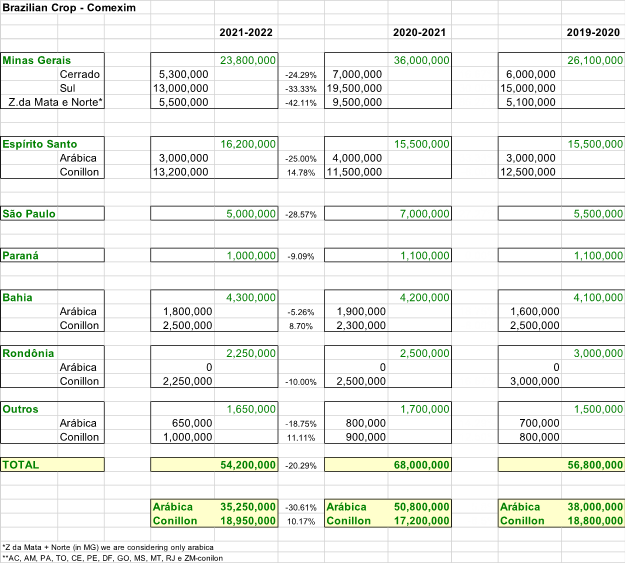

The impact of the below average rainfall and high temperatures in Brazil have been widely circulated in the market. Perhaps we are bit less pessimistic than others, but there is no doubt that the 21/22 crop potencial will suffer as a result. We see Mogiana as the region that has been hit the hardest, and while weather conditions have improved, it was a bit too late to reverse to completely reverse the situation. The weather impact coupled with the bi-annual off-cycle will inevitably lead to a reduction to a much greater tune than the market was forecasting months ago.

With that in mind, for 2021/2022 we are forecasting 53.7 million bags, split 35.2 for arabica and 18.5 for robusta. This would imply 30.7% reduction in the arabica crop and a 7.5% increase in robusta.

A global supply and demand deficit for 2021/2022 is pretty much the consensus, but again the size of this defecit will largely depend on demand and consumption and the pace at which countries can implement their vaccionation programs and get their economies back to whatever the “normal” will look like.

Exports from Brazill will naturally fall as a result of this in the 21/22 period, and we are estimating approximately 38.3 million bags (a 15% reduction), however we believe that this year’s ending stocks, both at origin and destination will be drawn down to extremely low levels as a result. In Brazil for instance, and according to our estimates, we would end up with a carry-over for 21/22 of 1.1 million bags.

This may all sound doom and gloom, but we largely believe that these numbers are already priced into the market, for the most part, and these forecasts will largely play out in the differentials. That being said, we are supportive to mildly bullish flat price.

Lastly, we are pleased to share that our European subsidiary is already in the final stages of incorporation and we hope to share more news with you all on this in the very near future.

The next pages includes the data tables containing the numbers we’ve discussed in this report, and we remain at your disposal should you require any additional clarifications or wish to discuss further.

Stay safe and Best Regards from all of us,

Team Comexim