Crop Report 2026/2027

Santos, march 11th, 2026

Dear Coffee Friends and Partners,

While taking a moment to prepare this report, we cannot help but to reflect on several topics and how things have evolved over the past year or so. At time of writing last year’s report, in parallel to the then ongoing conflicts and geopolitical tensions, the coffee sector was grappling with an unprecedented rally that took the terminal prices to historic levels, US’ tariffs came on and off, and EUDR had been postponed again, just to mention a few noteworthy facts.

Fast forward to today, and the outlook for coffee is starting to tell a different story to what we have seen over past several crop cycles. Forecasts seem promising, terminal prices have retreated from all-time highs, inverted price structure has softened; while on the other hand consistent protectionist policies and geo-political tensions along with existing, enduring, and new conflicts, are testing the robustness of our global and integrated supply chains.

It’s that time of year when crop forecasts are being fine-tuned and are slowly making their way around the market. All eyes are on Brazil and the expected output for the 26/27 season, which starts to harvest in a few months-time. Forecasts for the new crop do not appear to be as wide-ranging as seen in previous years, indicating a bit more of a consensus amongst market participants. And it does look promising indeed.

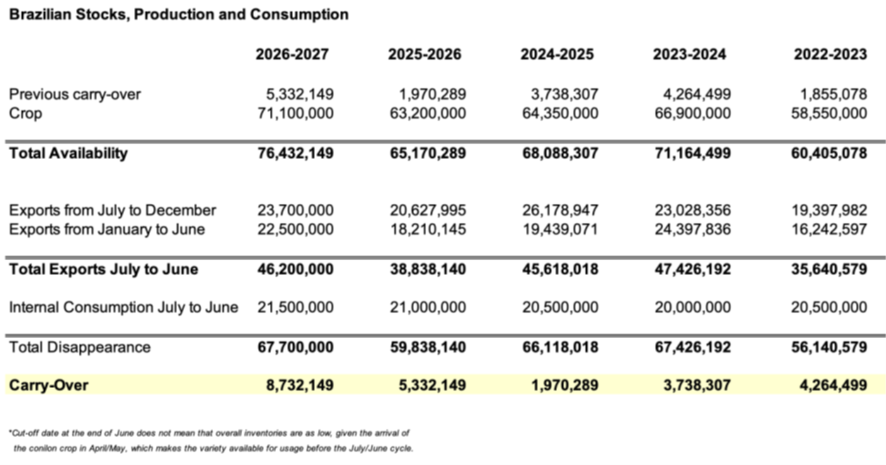

Before looking at new crop estimates, let’s quickly glance back at our original projections for this current 25/26 cycle. Our last report estimated a total crop of 63.20 million bags for the current season, composed of 39.90 for arabica and 23.30 for robusta, with total exports of approx. 45 million bags. Exports have been lagging and are below our original forecast. They are now estimated to reach just below 39mln bags for the 25/26 season. While we have not adjusted our total crop number, the composition is now of 37.70 mln bags for Arabica and 25.50 for Conilon (a shift of 2.20 between the two). We are of the opinion that these adjustments better reflect the ongoing market dynamics (more usage of Conilon in the domestic market, lower exports overall, and tight Arabica differentials).

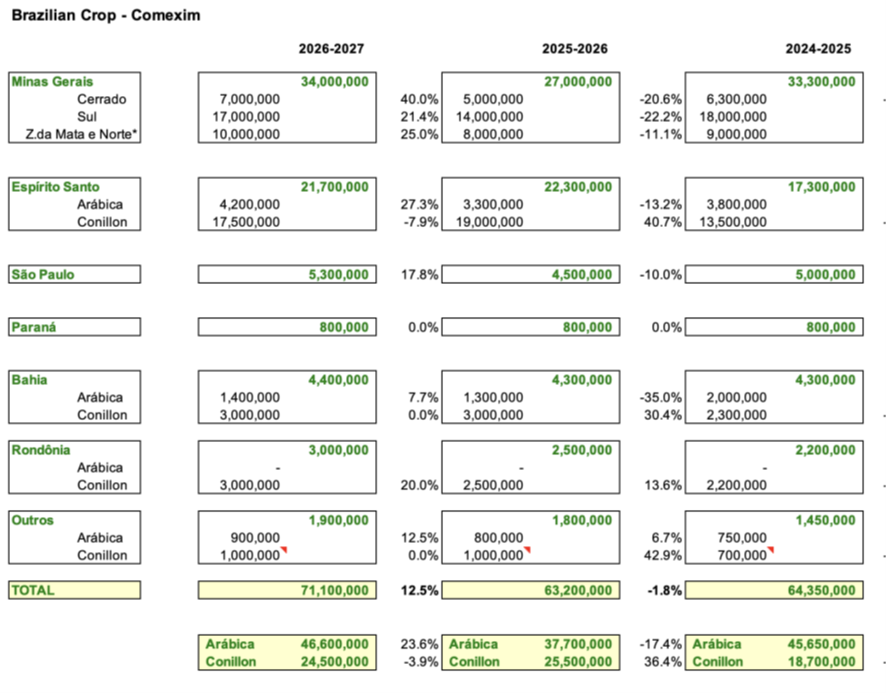

For the upcoming 2026/2027 crop season, despite mixed results between Arabica and Robusta, we are seeing a significant increase in the overall crop size when compared to this season. In arabica, we see increases in all the producing regions, leading to an estimated 46.60 million bags of production (a 23.6% increase). Robustas (Conilon) paint a different picture, with increases in some of the expanding areas in Rondonia, etc, but a small decrease in Espirito Santo, the main region, and thus resulting in a production estimate of 24.50 million bags (a very decent size by all accounts but a decrease of 3.9%).

This gives us a total production estimate for the new crop of 71.10 million bags, and an overall increase of 12.50%, or a 7.90 million bag growth vs the current season. (Please refer to the below tables in the appendixes). We estimate an expansion in exports for the next season at a similar proportion to the surge in crop size; in numbers approx. 46.20 million bags. Resulting from a probable uptick in domestic consumption to 21.50, we calculate the carry-out stocks to be around 8.60 mln bags. (pls refer to the tables in the appendixes)

Total exports for the 25/26 season will end-up lower than in previous years, and less than we originally anticipated, thus leading to a larger than previously estimated carry-over stock; reflecting the high capitalization levels at farm-gate we previously discussed. But, on the other-hand, this leaves a higher amount of current crop that will transition and eventually join the on-set of the new crop.

The new crop will begin to flow a bit early this season and we expect some regions to begin harvesting towards end of April / early May. While we are seeing light at the end of the tunnel in the medium to long-term horizon; as the coffee remains in the hands of very well capitalized producers, we expect the current tightness in BR differentials to continue for the short-term amid a retreating market, and until the flow of the new season.

To conclude, the market consensus is that the large crop expected for 2026/2027 will tip the global supply/demand balance into a surplus, and as a result would expect to re-stocking of global supplies following several seasons of drawdowns.

We remain at your disposal should you wish to discuss the above in more detail or require further clarifications.

Keep well and best regards from all of us,

Team Comexim

Appendix 1.

Appendix 2.

Disclaimer: The information contained in this report is provided for general informational purposes only. While we endeavor to keep the information up to date and correct, we make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the report or the information, products, services, or related graphics/charts contained in the report for any purpose. Any reliance you place on such information is therefore strictly at your own risk.

In no event will we be liable for any loss or damage including without limitation, indirect or consequential loss or damage, or any loss or damage whatsoever arising from loss of data or profits arising out of, or in connection with, the use of this report.

Every effort is made to keep the website up and running smoothly. However, we take no responsibility for, and will not be liable for, the website being temporarily unavailable due to technical issues beyond our control.

We reserve the right to update or remove any information contained in this report as deemed necessary.